|

|

|

|

|

|

|

|

|

Brazilian Gold and the Lisbon Mint House (1720–1807)*

Rita Martins De Sousa

Gabinete de História Económica e Social

Instituto Superior de Economia e Gestão

Universidade Técnica de Lisboa

[email protected]

Abstract

The purpose of this article is to present the official registers of the arrival of Brazilian gold in Portugal, the Livros dos Manifestos do 1% do ouro do Brasil, which are part of a documentary database that exists at the Lisbon Mint House. Discussion of this source and the data provided by it can contribute towards a better historiographic understanding of the issues related to precious metals. The intention here is also to make a comparative analysis between the statistical series already available about the flow of gold across the Atlantic to Portugal and the data available about Spain, facilitating comparisons between the production of the official sources for gold and silver in the two countries. Contrary to what happened in the case of the Casa de la Contratación, which lost control over cargoes after 1668, the Portuguese legislation always afforded the Lisbon Mint House a relatively centralizing role in the receipt of gold remittances.

The first section of this article describes the institutional framework behind the source of the Livros dos Manifestos, making a comparison with Spain, which did not lose its relative homogeneity in spite of the changes introduced through legislative procedures. In the second section, a comparison is made between this official source and the results provided by other statistical series describing gold flows at that time.

The period under scrutiny is that between 1720 and 1807. The beginning of this time scale is explained by the centralization policy introduced in 1720 when a 1% tax first began to be levied on the value of the gold shipped to Lisbon. The Livros dos Manifestos ended in 1807, when gold ceased to be a source of tax revenue for the budgets of the Portuguese state.

Keywords

Precious metals; Brazilian gold; Lisbon Mint House; Casa de la Contratación

Resumo

Neste artigo apresenta-se os registos oficiais das chegadas de ouro a Portugal, Livros de Manifestos do 1% do ouro do Brasil, que fazem parte de um acervo documental existente na Casa da Moeda de Lisboa. A discussão da construção desta fonte, assim como os dados por esta disponibilizados contribuem para o aperfeiçoamento do conhecimento historiográfico das temáticas relacionadas com metais preciosos. Perspectiva-se uma análise comparativa com as séries até agora disponíveis sobre os fluxos de ouro que atravessaram o Atlântico. Este estudo comparado amplia-se, em termos do processo de construção de ambas as fontes oficiais, às séries da prata disponíveis para Espanha. Contrariamente ao ocorrido na Casa de la Contratación que perdeu o controlo dos fluxos de prata chegados a Sevilha depois de 1668, a legislação portuguesa conferiu sempre à Casa da Moeda de Lisboa um papel relativamente centralizador sobre os fluxos de ouro brasileiro.

Na primeira secção deste artigo apresenta-se o enquadramento institucional de produção dos Livros de Manifestos que, apesar de algumas alterações legislativas nunca perdeu a sua relativa homogeneidade. Na segunda secção confrontam-se os resultados sobre os fluxos de ouro obtidos através dos Livros de Manifestos com os apresentados em diversos estudos a partir de outras fontes.

Os limites temporais situam-se entre 1720 e 1807. O início do período explica-se pela política de centralização introduzida em 1720, quando a taxa de 1% passou a ser cobrada sobre o valor do ouro remetido para Lisboa. Os Livros de Manifestos finalizam em 1807 quando o ouro deixou de ser uma fonte de receita nos orçamentos do Estado Português.

Palavras-chave

Metais preciosos; Ouro do Brasil; Casa da Moeda de Lisboa; Casa de la Contratación

“(…) gold (…) a barbarous relic”

(John Maynard Keynes, A Tract on Monetary Reform)

Introduction

One of the themes developed in the international historiography of the Atlantic shipping system is related to the trading of precious metals between the 16th and 18th centuries. The effects that this trade had on the movement of prices (from Hamilton, 1934, to Flynn, 1996), the fluctuations of the Iberian and Latin American economies (Romano, 2004), the monetarization and growth of the European economy and the decline of the Iberian states (Drelichman, 2005b) are merely a few of the ongoing research topics.

However, it is the remittances of silver, rather than those of gold, that have tended to dominate European and Latin American historiography.1 The study of the Brazilian gold remittances has been deeply influenced by the theme of Anglo-Portuguese relations (Sideri, 1978; Fisher, 1984). The main aim has been to explain how England not only played a crucial and central role in international payments during the 18th century but also accumulated sufficient reserves of this precious metal to be able to adopt gold monometallism at an earlier date, in 1821 (Redish, 1990). In turn, Portugal has traditionally been seen as a peripheral economy in Europe through which gold passed without this process having had any long-term economic consequences. The gold flows are deemed to have had merely short-term effects, with two particular short periods having been identified and chronologically situated in the first and second halves of the 18th century. The first half of the century is thus presented as displaying a rising trend in remittances as gold production increased, while during the second half of the century the decline in production led to a decrease in remittances from across the Atlantic, causing a downward trend and leading to a crisis in the Portuguese economy. The studies by Macedo (1982 and 1989), together with those by Vitorino Magalhães Godinho (1955), discovered a direct association between gold flows and short-term economic trends.

|

Recent studies have shifted the emphasis given to Brazilian remittances by exploring monetary approaches. An assessment has been made of the effects of gold remittances on the supply and circulation of money in Portugal in the 18th century. It can be concluded that, despite the fact that the trade deficit with Great Britain drained off a lot of the gold, part of the supply of this precious metal nonetheless caused the sustained rise in prices, the increased level of monetarization of the economy, and also a probable increase in hoarding in Portugal during the 18th century (Sousa, 2006).2

All of the studies made to date that needed to assess information on Brazilian gold flows in order to make their calculations and reach their conclusions used as fundamental references the studies by Virgílio Noya Pinto (Pinto, 1979) and Michel Morineau (Morineau, 1985). Consular correspondence and the information recorded in the Dutch Gazettes were the sources used, which in the case of Morineau’s studies continued until 1788. Essentially basing his findings on consular correspondence, Noya Pinto stopped at the beginning of the 1760s, justifying his decision by the fact that after 1765, the date when the fleets were brought to an end, diplomatic correspondence did not provide accurate information on the evolution of the rhythm and rate of gold arrivals in Portugal. As far as Morineau’s data are concerned, despite the fact that the series of the Dutch Gazettes continued until 1786, the author stresses that the free navigation system brought into force as early as September 1765 had disorientated the Gazette writers.

The existence of an official fiscal source, the Livros dos Manifestos do 1% do ouro do Brasil, can be added to the consular and trading information. Godinho’s pioneering article, Frotas do açúcar e frotas do ouro, dating from 1950, mentioned these ledgers. Godinho’s data were recently made available and included in a Master’s Degree dissertation (Lopes, 2001). This has resulted in the publication of the untreated data up to 1736 and for the isolated year of 1740. The quantity of information provided by the registers in the Livros dos Manifestos made their exhaustive study a lengthy process, which could only be carried out with a team of researchers and appropriate IT support.3 Russell-Wood (1983) explained the source to researchers and underlined the importance of the data.

The Livros dos Manifestos extend the period of analysis beyond the decade of 1760 and provide a much broader set of data than just the annual total of these remittances. These data afford answers to three fundamental questions: how much gold arrived in the state’s coffers? Is there any connection between the fiscal trends of gold flows and the amounts sent by private economic agents? What can we learn from a comparison of the data obtained from the Livros dos Manifestos and those presented in previous studies (Noya Pinto, 1979; Morineau, 1985)? Furthermore, if one considers the gold that arrived (worked gold, dust, bars or coins) and the agents involved, the exploration of this source opens up a wider range of issues than those raised by previous approaches.4

The decision to make a systematic study of this official source is justified by the controversy that arose in Spain when an identical source was used. The crisis in the remittances that occurred in the second half of the 17th century, first noted in Hamilton’s study (Hamilton, 1934) and later reiterated by other authors (Ortiz, 1969), resulting from their analysis of the official records of the Casa de la Contratación, was contradicted by the Dutch Gazettes, according to the information provided by Michel Morineau (Morineau, 1985). Thus, depending on the sources used, official or otherwise, the history of the remittances of silver can be recounted in completely different ways. The explanation for such a discrepancy is related to the nature of the official records of the Casa de la Contratación, since after 1660 changes in the law meant that the recording of silver remittances became optional (Melgar, 2005).

In this article, I intend to go further in searching for reliable data of gold flows. The Livros dos Manifestos are examined in an attempt to obtain more accurate data about gold remittances, which in turn can contribute towards a better historiographic understanding of the issues related to precious metals, namely, a reassessment of the economic impact of the gold remittances from Brazil on the Portuguese economy. A comparative analysis is also made between the data already available about gold remittances to Portugal and the official Spanish sources of data about gold and silver. Contrary to what happened in the case of the Casa de la Contratación, which lost control over cargoes after 1668 (Melgar, 2005), the Portuguese legislation always afforded the Lisbon Mint House a relatively centralizing role in the receipt of gold remittances. As we shall explain further on, the control that was taken of this business by the Portuguese State resulted in an important collection of documents, which still remain in the archives of the Lisbon Mint House.

The first section will be devoted to describing the institutional framework of the Livros dos Manifestos, simultaneously making a comparison with Spain, which did not lose its relative homogeneity in spite of the changes introduced by legislative procedures. In the second section, a further comparison will be made between the conclusions obtained through this official source and the results already provided by other studies.

The period under scrutiny is that between 1720 and 1807. The beginning of this time scale is explained by the policy of centralization that was introduced in 1720 when a 1% tax first began to be levied on the value of the gold transported across the Atlantic Ocean. The Livros dos Manifestos ended in 1807, a fact that is not unconnected with the transfer of the Court to Brazil in the following year. For a few years, Lisbon ceased to be the Empire’s central place of reference and a new cycle had begun. Gold ceased to be a source of tax revenue for the budgets of the Portuguese state.

1. The production of the official source: Livros dos Manifestos

The payment of the 1% levy on gold was recorded in the Livros dos Manifestos do 1% do ouro do Brasil, which used to be carried on the carracksescorting the fleets. These books were later kept in the Lisbon Mint House, where the gold carried on ships coming to Portugal had to be taken. Despite the fact that the system of sailing in fleets finished in 1765 (Charter of September 10), the series continued until 1807. The need for the fiscal control of precious metal cargoes explains this continuity.

From 1720, the Manifestos, ledgers written by scribes traveling on the carracks of the fleet, registered the remittances of gold belonging both to the private agents and to the state. Those transporting gold under the system of compulsory escort paid 1% to the Lisbon Mint House. This levy was paid when the recipient (either in person or represented by his proxy) collected the gold sent from Brazil. This tax was fixed and justified by custom, for it was written that “the payment of a 1% commission was customary for Masters and Officers of Merchant ships.”5 In this way, the payment of the tax was based upon a common practice in the transportation of goods.

This 1% payment on the gold transported also marks a turning point in the quality of the source. Despite the fact that the Livros dos Manifestos had existed since 1711, not only did these not exist in a printed form, but the number of books sent was also insufficient to ensure the recording of all the quantities of gold brought from Brazil. Apart from this, the ledgers kept until 1720 were not homogenous, since some scribes kept them in chronological order, while others kept the registers in alphabetical order, sometimes starting with the sender and on other occasions with the agent (Russell-Wood, 1983: 705). In this way, the payment of the 1% tax not only instituted a greater control over the gold which arrived in Lisbon, but it also made it compulsory to keep the registers in accordance with a printed model.6 The gold was carried in safes and therefore each Livro de Manifestos (see Figure 1) referred to a safe in which two hundred or more deliveries of gold were kept. The permission to transport gold outside the safes, granted in February 1736, did not imply any alteration in these ledgers, for these merely referred to such gold through the expression “outside safes”. In this case, the captains or other officers of the ship received the 1% beforehand at the time of departure from Brazil or when the gold was presented on board the carracks. This tax was delivered at the Lisbon Mint House when the fleets arrived. However, the permission to transport gold outside safes was limited to either gold coins or worked gold.

The organization and type of entries made in the Livros dos Manifestos make it possible to obtain a complete set of information about the gold circuits: the ports of origin—Rio de Janeiro, Baía, Pernambuco, and after the 1750s also Grão Pará and Maranhão, Pernambuco and Paraíba—the name of the carrack and the vessels, and a complete report of the final delivery with a vast range of information both in quantitative and qualitative terms. The quantitative information covers the quantity of gold carried and the form it took—worked gold, dust, bars or coins—regularly specifying the number of coins and their face value. The qualitative information organized data according to the agent(s) involved in each remittance – sender, recipient(s), proxy(ies). This source allows us to consider two main aspects: a study of the management of the networks of merchants involved in gold flows and a quantitative approach to the remittances received either by the state or by private agents. This separation of the recipients gives us new leads into the study of other themes, such as the fiscal costs incurred in colonies during the mining period, as well as a reassessment of Atlantic and Portuguese fluctuations related to the influx of gold.

The aim of this section is circumscribed to the way in which the source of our data was kept and built up and to the explanation of its continuity after the end of the system of an escorting fleet. A comparison with Spain allows us to explain the particularities of the Portuguese source.

The changes in the administrative framework responsible for the delivery of gold remittances and the changes in the shipping systems, above all after the 1760s, did not alter the homogeneity of the source throughout the period, as will be demonstrated in the following paragraphs.

As for the administrative framework involved in the collection of the tax, from 1757 onwards, successive resolutions and decrees regulated the procedures related to the act of receiving gold in Lisbon. For example, some of the functions that were attributed to the traders involved in this activity included delivering remittances and acting as trustees of the Manifestos in the safes at the Mint House, as well as depositors of the remittances which were not handed over due to the recipients being absent.7 These institutional changes placed merchants among the bureaucratic staff responsible for collecting the 1% tax. These were businessmen appointed by the Junta do Comércio (Board of Trade), set up in 1755. The increasing importance of merchants during the second half of the 18th century can also be seen from their overwhelming proportion among minters (71.8%) who supervised the gold network in the Mint House (Sousa, 2006: 41-49). Therefore, after the setting up of the Junta do Comércio in 1755, the influence of the merchant group increased, although the taxation on gold, managed by the state, remained unchanged.

As for the changes in shipping procedures, this did not imply a total modification of the source, because the state found other administrative mechanisms for controlling the gold flows which crossed the Atlantic. Until 1765, this control system was facilitated by the existence of a fleet system representing the payment of a 1% tax on the value of gold—considered as a protection cost (Costa, Rocha and Sousa, 2005). This tax was similar to other freight charges practiced at the time for precious metals. In the Portuguese and London markets, there were percentages of between ¼% and 1% charged on the value of the gold and silver transported, the freight charge being higher in the case of warships, where the limit of 1% was reached (Fisher, 1984; Sutherland, 1962). The transportation costs for the London-Paris and London-Amsterdam routes in the 18th century were estimated at between 1% and 1.5%, respectively (Boyer-Xambeu et alii, 1994; Quinn, 1996). Thus, the payment of the 1% tax in Lisbon on the gold sent from Brazil represented a risk coverage that was less than the cost of losing a ship with highly valuable merchandise.

In 1765, the fleet system was brought to an end,8 allowing for gold to be transported in vessels outside the fleet and therefore outside this form of protection. As soon as the fleet system was ended, vessels laden with gold remained in the Brazilian ports, claiming that they did not have the means to transport such valuable merchandise in safety. The absence of safety in transporting gold across the Atlantic was given as the reason why the precious metal did not arrive in Portugal. It is not possible to prove the veracity of this statement presented by the state in the Edict of June 10, 1766, although this was the explanation that legitimized the departure thereafter of two war frigates per year from the port of Lisbon to Rio. The first left in April and stayed in Rio for one month, then continued on to Baía, where it stayed for two more weeks. The second frigate, which left the port of Lisbon in October, spent one month in Rio and came straight back to Lisbon. These frigates received and transported all the remittances belonging to the state, and if private agents wished to use this shipping service they were also allowed to deliver their remittances to the Royal Officials. In all cases, they had to pay the 1% tax at the Lisbon Mint House.

As was the case with any other merchandise, the arrivals of gold were submitted to customs procedures. This does not mean that all the gold which entered the ports was declared—fraud would most certainly have existed. As some studies have demonstrated, fraud and contraband were an integral part of the process of precious metal circulation (Pijning, 2001; Melgar, 2005). Nevertheless, a systematic checking procedure sought to minimize this. In this way, one can explain the existence of a great deal of separate documentation, namely the “Visita do Ouro” (Gold Inspection) made by the Inspectores do Cofre (Inspectors of the Safe) on the ships which arrived in the port of Lisbon. Any gold that was not declared in the captain’s log was confiscated.9 In spite of these efforts to control contraband, a Royal Charter in 1770 recognized that the remittances of gold sent on merchant vessels increased after 1766, ignoring the role of the frigates. Some of this goldcould therefore have escaped the recording of the 1% payment, since there was competition for its transport between the frigate system and a free transportation system. The commission of 1% on the frigates was higher than the 0.5% commission received by the gold carriers. Given this situation, the Royal Charter decreed that the state would share the 1% in equal parts with the person(s) that declared the value of gold transported (captain, master of the ship or pilot). All captains of merchant vessels who wished to transport money or gold bars from Brazil and had applied to receive 0.5% after registering the gold would be obliged to take a safe with three keys to the destination port; these keys would be given to them at the Lisbon Mint House. The delivery of the gold sent in this way required the signatures of the captain, the master of the ship and the pilot, these being the only officers authorized to register the remittance in the Manifesto. Dividing the tax in this way allowed the state to exercise greater control over the gold which arrived, because the less the captains declared, the less they received.

These different means of transportation practiced by the private agents explain why, at the Lisbon Mint House, there were separate Manifestos, in addition to the Livros dos Manifestos which were carried in the war carracks after 1765.10 The state continued to send its net revenue in the war frigates and, with these protection mechanisms, private agents were encouraged to register their gold. The option of private agents to register the transported gold can be assessed at the outset from a study of the number of registers made and the value of the gold carried. Between 1766 and 1807 there are around 34,500 entries made in the Livros dos Manifestos carried on board the frigates (which corresponded to around 55,700 contos, 38,521 of which was accounted for by private economic agents), against just 2,550 entries in the loose Manifestos (which represented 12,500 contos). On the other hand, a significant quantity of gold was recorded in the loose Manifestos, relating to gold sent from Bahia and with Porto or other cities in the north of Portugal as its destination. In this way, the end of the fleet system and the greater freedom in transporting gold implied that the state had set other mechanisms in place for shipping gold, which explains the continuity of the source after 1765.

This does not mean that the information contained in the Manifestos tells us everything about the gold that was carried because they only refer to the gold which arrived through official circuits. However, according to the Brazilian royal officers’ correspondence, while wary of discovering fraud during the crossing of the Atlantic to Portugal, they actually found that contraband and fraud were more frequent in Brazilian territory. At least some of this fraud was perpetrated in order to escape the payment of the quinto.11The route Brazil–Northern Europe–Western Africa was also used for contraband (Russell-Wood, 1983: 709). However, among the various taxes imposed on gold (1%, seigniorage, quinto), the 1% tax was paid on delivery. Russell-Wood comments that “the simple threat of punishment was often enough to get the sailors, travellers, passengers or even the captain, to make their declarations or modify those which had been made previously on the high seas” (Russell-Wood: 1983: 703). Nevertheless, these threats did not eliminate fraud, and so the Manifestos certainly did not record all the gold which arrived in Lisbon, even if some of these frauds had been detected and thus turned into cases for legal action. In the books known as the Registo Geral and the two books of Tomadias e Sequestros12 at the Lisbon Mint House, there are some references to attempts that were made to escape the payment of the 1% tax, although their extent and the amounts involved were not significant in the general context of gold flows.13

Contraband existed in Europe and in the European colonies and, in this sense, it also played a part during the various phases when precious metals passed from production to final destination (Boxer, 1969: 460–64).14This was inherent in the economic system (Pijning, 2001) and its study implies another theoretical matrix, other sources and methodologies.15

However, if the flows of silver in the 17th century gave rise to criticism about the relevance of official sources for adopting a quantitative approach to the question of precious metals being transported from America to Europe (see Morineau’s research based on the Dutch Gazettes), the Portuguese official records stem from a different institutional framework, which may be considered to provide accurate information, as will be explained throughout this paper.

The poor quality of the registers at the Casa de la Contratación from 1660 onwards stems from a legislative framework that brought an end to the compulsory keeping of records of silver transactions and their entry in the Casa de la Contratación.16 The Spanish Treasury also renounced the levying of various taxes on the Carrera de las Índias (India Route), namely the almoxarifado, and the avería,17 replacing them with a fixed annual contribution.18 In the same decade, after 1668, the officials of the Contratación ceased to be responsible for signing for the return cargoes. The Consulado not only managed to reserve for itself the right to recognize the return cargoes on the fleets but also took it away completely from the Casa de la Contratación. The Consulado took on the position of fiscal agent and intermediary between the merchants and the state. The power of these merchants means that the Spanish state did not always centralize the process of silver remittances from America and gave up its supervisory position with regard to the silver trade to the judicial bodies which represented private interests.

In Portugal, merchants also had institutions to defend their interests: Mesa do Bem Comum dos Homens de Negócio, followed after 1755 by Junta do Comércio destes Reinos e seus Domínios, which was transformed in 1788 into the Real Junta do Comércio, Agricultura, Fabricas, e Navegação destes Reinos, e seus Domínios. However, these merchant associations never led to the formation of a corporative body such as the one developed by the Spanish Empire and these institutions were not fiscal agents.

These diverse institutional settings created different paths for the flow of precious metals to follow. In Spain, besides the state having renounced fiscal control, other differences can be detected regarding the level of centralization in the reception and coining of metal. In Portugal, the process to register and receive the Brazilian gold was centralized and controlled by the state from the beginning. This centralizing process was coherent with the policy of the Portuguese State, because the monetary issues made by the Kingdom of Portugal were also centralized at the Lisbon Mint after 1714. This decade coincided precisely with the beginning of the great flows of Brazilian gold. In Spain, this centralization process did not occur during the silver century. Until 1728, Segovia, Madrid, Toledo, Granada and Cuenca were the Mint Houses that coined metal money, and only after 1728 were the distributional hubs of monetary issues reduced to Madrid, Segovia and Seville (Sindreu, 1992; Sousa, 2006). Other differences occurred throughout this process. While in Portugal it was possible for private agents to sell precious metal at the mint house, this was not the case in Spain during the 17th century. There were intermediaries between the private agents and the mint houses. More precisely, rich finance companies bought gold and silver and delivered the metals with the required carats to the mint house. This procedure was the norm until 1701, and only after that time were private agents able to go directly to the mint with the purpose of coining. This was the case even with the king’s metal, which could be coined directly at the mint house or sold to gold and silver traders (Anes, 1996; Sindreu, 1992). In Portugal, during the 18th century, the king sent almost all the gold received from Brazil to be coined at the Lisbon Mint House (Sousa, 2006).

In Portugal the centralized nature of trading activity in Lisbon19 also facilitated the maintenance of central control by the state. In the case of Spain, though Seville only lost the Casa de la Contratación and the Consulado de Mercadores to Cadiz in 1717 (decree of May 12, 1717, by Philip V), Cadiz had been the main port used by the Carrera de las Indias since 1680.

All these fiscal, monetary and administrative differences explain why the official ledgers of the Casa de la Contratación did not record all the instances of silver imports. Not only did silver registers cease to be compulsory, as we have already stated, but Seville was also merely an administrative centre from 1680 onwards (Anes, 1996; Ibarra, 2000; Melgar, 2005). This explains the different quality of the official sources regarding the quantities of precious metals which arrived in the two Iberian kingdoms. The official Spanish source is undervalued, for it ceased to record remittances after 1660. Thus, the re-assessment of the silver arrivals made by Michel Morineau from the Dutch Gazettes raises doubts as to the decline of the Carrera de las Índias in the 17th century and calls into question some of the historiographic theses that have been developed. The crisis in the Carrera de las Índias is no longer explained by the decline in the system itself but should be seen instead as a consequence of the progressive loss of control by the state (Morineau, 1985; Melgar, 2005).

In short, significant differences can be found between the ‘century of gold’ in Portugal and the ‘century of silver’ in Spain. In Portugal, the 1% tax continued until 1807 and was not confined to the period when the policy of navigating in fleets was the only way in which Brazilian ports could be reached. While Spain ceded its fiscal position to the Consulado, in Portugal the state opted to share the cost of the tax with the carriers if the metal was transported in merchant ships outside the frigate system. This administrative decision compelled private agents to send metal indirectly under the frigate system, because, for the same cost, they would have the advantage of greater security in transportation. In this way, if the 1% tax represented a protection cost until 1765, after the end of the fleet navigation system, it resulted in the involvement of the State with the carriers of the gold. For the private economic agents, the payment of 1% was maintained whether they shipped their gold in royal frigates or in private ships. The change occurred for the state, which started to divide the 1% tax with the captains of the vessels to force them to take a higher degree of control, while the gold was transported in private vessels. This can explain why, according to official sources, private agents chose military vessels, since the quantity of gold recorded in the Livros dos Manifestos and transported by frigates surpasses that of the loose Manifestos written whenever gold was shipped in private vessels. This had the advantage of not being subjected to fixed dates for a return voyage, although it displayed the disadvantages inherent in a lesser degree of protection.

2. Gold remittances: a comparative analysis

With the Manifestos, the sources used to calculate the quantities of Brazilian gold that arrived in Portugal during the 18th century may now be considered much more complete. The Manifestos need to be critically studied, taking into account the consular correspondence and the Dutch Gazettes. What are the differences between these documentary sources? Why are there differences in the amounts that they show?

To begin with the information sources on which certain studies in this area have been based, it is important from the outset to stress that some studies have tried to use official Portuguese sources:information from the Captaincies, official instructions sent to Brazil, and official maps containing varying items of information. The works by Boxer (1962; 1969) and the British Parliamentary Papers20 are significant examples of this procedure.

In the case of Noya Pinto (1979), this author uses several sources, although the main data are derived from the French Consular correspondence. For the missing years, Noya Pinto considered the work by the Viscount of Santarém, along with the account prepared by Vitorino Magalhães Godinho, who used the Livros dos Manifestos of 1% for the first time.

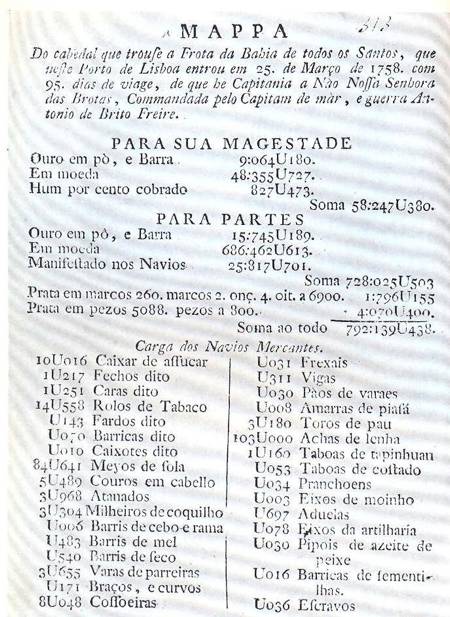

As far as the Dutch Gazettes are concerned, after the interest that they had shown in the sugar cargoes, the arrival of the first fleet laden with gold increased their curiosity about this “new” source of wealth. The regularity with which the transportation of gold took place therefore gave rise to the continuous publication of news between 1712 and 1760. However, according to Morineau, such regularity in the publicizing of the quantities of precious metals arriving in Lisbon is to be explained by the accessibility of information. In the description he makes of the gathering of information, he states that the final news published in the gazettes was based on several layers of information: the arrival of the fleets in Lisbon triggered rumors in the city about the amounts of gold received, to which hand-written messages were also added, originating either from the captains of the vessels or from another authority, and, finally, the Portuguese government authorized the printing of an official manifesto (what could, in fact, be called a list of the cargo—gold and other goods—that had arrived in Lisbon, known as the Mappa to differentiate it from the Livros dos Manifestos). This printing of the official Mappa (see Figure 2) of cargo arriving is explained as follows: “le gouvernement royal, au bout d’un délai variable, autorisait souvent l’impression des manifestes officiels. Tout le monde, sur place, pouvait se procurer ces documents, les recopier ou les dépêcher directement à l’adresse d’un correspondant étranger” (Morineau, 1985: 124). Thus, it appears that the official sources of information were those that everyone wanted to have access to in both the 18th and the 20th century. When Morineau states, “Lorsque le manifeste officiel figure parmi les notices, son chiffre a été adopté comme plancher pour l’évaluation des trésors” (Morineau, 1985: 133), he confirms that the information provided by the Portuguese government was fundamental.

In this way, it is supposed that the data originating from the gazettes, despite being similar to the consular information (which was worked upon by Noya Pinto), correct and complete these records,21 even if one cannot entirely discard the hypothesis “d’une défaillance simultanée des gazettes et des consuls” (Morineau, 1980: 125). And this mistake was a real one. One clear example is provided by the Baía fleet, which was missing in 1742–1743, both in the consular correspondence and in the gazettes, but was well reported by the Livros dos Manifestos at the Lisbon Mint House.22 Apart from this, although spanning the period from 1699 to 1788, the gazettes do not provide complete information for the period from 1770 to 1788 due to the fact that the beginning of the free navigation system on September 10, 1765, disturbed the information flows used by gazetteers. As information was missing for certain years, these missing years were built by linear interpolation based on the value of the fifth (quinto). This is calculated from the five-year average value of the royal tax levied on gold arriving in fleets from the same port of origin (Morineau, 1980: 133–35). On the other hand, the data obtained after 1770 in the Gazettes only represent “des fragments,” and so this led Morineau to justify his procedures when he used other sources.23

Figure 1. Livros dos Manifestos do 1% do ouro do Brasil, Lisbon Mint House Archive.

Figure 2. Mappa—a list of the cargo of gold and other goods transported in the Bahia fleet that arrived in Lisbon on March 25, 1758 (Boxer: 1969).

In the case of the Manifestos, the calculation was systematic and there was no extrapolation or estimation. The information contained in these Manifestos was merely completed by documentation about the arrivals of gold in merchant vessels when the free navigation system was in force (see section 1). This is why the values recorded in separate Manifestos at the Lisbon Mint House between 1763 and 1807 were also calculated.24 In the case of the companies, Grão Pará and Maranhão, Pernambuco and Paraíba, which were not obliged to pay the 1% tax,25 the data were obtained from the separate Manifestos and, in the case of Grão Pará, this information is also to be found in the Arquivo Histórico Ultramarino.26

Through the Livros dos Manifestos, the calculation of the gold remittances results in an amount of 270,803 contos27 between 1720 and 1807. Of this total, 77.5% (around 210,000 contos) was destined for the private agents and 22.5% (approximately 61,000 contos) was for the state.

This calculation is based on certain methodological options, namely those relating to the conversions used and the quantities itemized under the heading “state”.

As far as the conversions are concerned, we adopted the same value for the different types of gold transported for the entire period under study. The stability of the legal price of gold between 1688 and 1822 made it possible to keep to this value, which stipulated a price of 96,000 réis for a mark of gold dust or gold bars and 89,600 réis for a mark (1400 réis per eighth) of worked gold (Law of August 4, 1688). The coins shipped to Lisbon were not subjected to any other conversion, given the fact that the source does not always make their face value clear. The methodology used, therefore, consisted of converting the quantities (marks, ounces, drams, grams) into values (contos) plus the face value of the coins received. Godinho (1990) and Boxer (1962) also used this method in their conversions, because the conversion pattern had to be based on the price of gold paid at the Mint House, which was fixed in 1688.28

The other conversions of weights and measures adopted in this paper were based on the use of Noya Pinto as a guide, except for the value of the cruzado, because this author assumes that it was worth 480 réis, which was the value of the gold coin called the cruzado novo. The correct value of the conversion must be 1 cruzado = 400 réis, because the cruzado was used as a monetary unit (Noya Pinto, 1979: 335).

Morineau’s conversions reveal differences which can be significant in the general context. In Incroyables Gazettes (1985: 132–33), the weight of gold transported is estimated from the quantity theoretically contained in a cruzado (0.817 grams). Therefore, 1 kg was assessed as being worth 1,225 cruzados.29 If we consider the unchanged legal price of gold between 1688 and 1822, this means that marks of gold in melted coins had a differential of 10,300 réis/marks and the gold in bars and dust had a differential of 16,700 réis/marks.

The quantities of gold which crossed the Atlantic destined for the state represented not only the patrimonial rights of the Portuguese Crown over a part of the gold mined in Brazil, but also other sources of income for the Royal Exchequer. In the Rio de Janeiro fleets, or when these finished in the war carracks which sailed from there, identification was facilitated because there were ledgers that had separate entries for ‘His Majesty’. For the other fleets (Baía, Pernambuco), the royal entries are found among all the other entries for the private agents despite often being marked with the word Rei (King) in the margin. The diversity of income covered in these ledgers is shown by the different terminology of their titles, which ranged from Sua Magestade (His Majesty) to Conselho Ultramarino, Tesoureiro da Fazenda Real,30 Tesoureiro da Casa da Moeda de Lisboa,31 Tesoureiro da Casa da Índia, Tesoureiro da Junta do Tabaco,32Tesoureiro de Defuntos e Ausentes, Mesa da Consciência e Ordens,34 among other entities related with the state (such as the Junta do Depósito Público). All of this points to some of the changes that were introduced into the central administration during the 18th century. The type of income received justified this wide range of recipients. Apart from a tax on the gold that was coined, the Mint Houses in Brazil allowed for the collection of other types of income, namely seigniorage.35 Income from the Customs Houses, contracts, and certain other taxes are among the sources of the state’s net fiscal income.

A comparative analysis allows us to calculate the relative importance of each of the gold sources. As far as the overall value contained in the Manifestos (270,803 contos) is concerned, this is an intermediate value between the amount calculated by Noya Pinto (190,922 contos) and that provided by the Dutch Gazettes (323,051 contos), even if it must be stated that these values represent different time spans. Another source sometimes considered as a reference in these analyses is the Gazeta de Lisboa, but between 1720 and 1759 its entries totaled a paltry 37,412 contos. In a comparative analysis of different five-year periods, we obtain the following results:

Table 1. Brazilian gold remittances, 1720–1807

(in contos)

5-year periods |

Manifestos |

Dutch Gazettes |

Consular Correspondence |

Gazetas de Lisboa |

1720-1724 |

15344 |

22259 |

27530 |

6518 (3) |

1725-1729 |

25210 |

41276 |

18938 |

|

1730-1734 |

20754 |

40219 |

26743 |

|

1735-1739 |

19405 |

29273 |

23486 |

|

1740-1744 |

28267 |

30137 |

28772 |

|

1745-1749 |

25957 |

30257 |

31036 |

6612 (4) |

1750-1754 |

26328 |

27010 |

24149 |

12372 |

1755-1759 |

21139 |

25612 |

8587 |

11910 |

1760-1764 |

18443 |

18340 |

1682 (2) |

|

1765-1769 |

19210 |

15668 |

|

|

1770-1774 |

15380 |

12000 |

|

|

1775-1779 |

11060 |

17760 |

|

|

1780-1784 |

8727 |

10040 |

|

|

1785-1789 |

1653 |

3200 (1) |

|

|

1790-1794 |

1316 |

|

|

|

1795-1799 |

4928 |

|

|

|

1800-1807 |

7683 |

|

|

|

Source: Manifestos, Livros dos Manifestos, Manifestos Avulsos, ACML and Livros das Frotas do Grão Pará, AHU; Dutch Gazettes, Michel Morineau, op. cit., pp 135-137 and 194-195; Consular Correspondence, Virgílio Noya Pinto, op. cit., pp 248-253; Gazetas de Lisboa, Lopes, op. cit, 2001, p. 13 (Appendix).

Notes:

- This figure covers the period 1785–1788.

- This corresponds to the year 1760, when the values used by Virgílio Noya Pinto come to an end.

- This figure is limited to the 2-year period 1720–1721.

- This corresponds only to the year 1749.

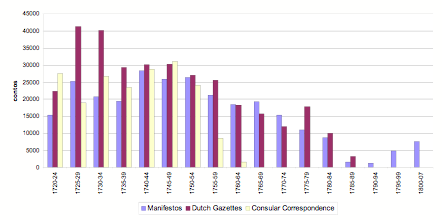

A comparison of the values over a five-year period shows from the outset that the Gazeta de Lisboa presents data which are not only very sparse, but also not very consistent. The differences between the sources—official, consular or derived from the gazettes—highlight the precariousness of the information gathered from the gazettes.

An analysis of Table 1 and Chart 1 reveals that the greatest differences between the other three sources can be found in the period from 1725 to 1734, with the gazettes registering far higher gold flows than the Livros dos Manifestos. In this period, the year 1731 is the one in which we can note the greatest difference between the series—13,135 contos in the gazettes versus 4,401 contos in the Livros dos Manifestos.

Calculating the gold production through the values presented by Noya Pinto (1979), we can conclude that, between 1726 and 1734, the production was 79,000 kg (33,000 contos) while, according to the Dutch Gazettes, around 140,436 kg (81,500 contos) of gold arrived in Lisbon. According to the Livros dos Manifestos, gold flows in the same period amounted to approximately 89,700 kg (37,460 contos). One must question how the value stated in the gazettes can be justified other than through an over-valuation of Morineau’s estimates. A comparison with other sources confirms the idea of over-valuation, particularly if the comparison is the gold that entered the smelting-house and the Mint of Villa Rica of Minas Gerais, from 1724 to 1750 (Boxer, 1962: 336–37). In the 1730s, the amount of gold entering the smelting-house was no greater than would be normal for that time.

Therefore, even if we were tempted to conclude that the differences noted in the decades of the 1720s and 1730s between the gazettes and the Livros dos Manifestos might indicate the quantities of gold involved in contraband, the high levels presented by the gazettes do not have any satisfactory explanation when compared with other sources. Furthermore, the comparison of the two sets of data between 1720 and 1788 shows twenty-five years when the Livros dos Manifestos presented values that were higher than those obtained from the Dutch Gazettes (Chart 2). This conclusion calls into question the argument that the differences between the two sources could be explained by the recording of contraband in the gazettes. It should also be underlined that after 1765, when the navigation scheme changed, the gold remittances which arrived in Lisbon according to the official sources are higher than those presented in the Dutch Gazettes.

Chart 1. Comparative analysis by 5-year periods (1720–1807)

Chart 2. Years when the Livros dos Manifestos presented values of gold remittances higher than the Dutch Gazettes (1720–1788)

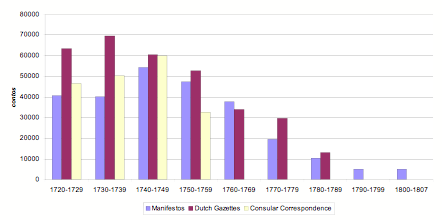

A study by decades, according to the gazettes, reveals that the periods with the highest quantities of arrivals were the decades of the 1720s and 1730s (especially the latter period), while according to the Manifestos, the decades which registered the greatest gold flows were the 1740s and 1750s. Therefore, the decades of the greatest remittances, according to the Livros dos Manifestos, coincided with the time span 1735–1754, the period of greatest gold production (cf. Chart 6).

Chart 3. Comparative analysis by decades (1720–1807)

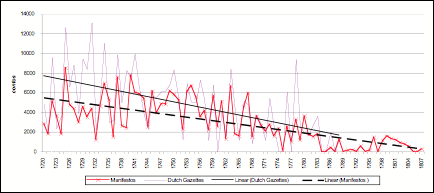

The behavior of the long-term trend reveals a marked decrease. In the case of the Dutch Gazettes, the values of the remittances oscillate between approximately 7,000 contos at the beginning of the period and less than 2,000 contos at the end. The Livros dos Manifestos tell a tale of greater stability, because the variation is smaller, being between 5,000 contos and slightly above 2,000 contos at the end of the 1780s (Chart 4).

Chart 4. Yearly analysis of remittances (1720–1807)

A general overview allows us to state that the Livros dos Manifestos not only present the 1740s as the period with the greatest quantities of gold arrivals but also reveal a greater long-term stability when compared with other series used in the historiography.

After the comparison with the other sources available so far, a first approach will be made towards treating some of the data collected from the Livros dos Manifestos.36

The gold remittances which arrived in Portugal totaled around 271,000 contos. This amount corresponds to an annual average of 3,080 contos, given that the GDP would be 200,000 contos in 1750 (Valério, 2001). The gold flows would have represented 1.5%/year if we take into account the whole period under study, or around 2%/year if we take into account only the period of greatest arrivals between 1720 and 1780. If we compare the state fiscal revenues collected between 1762 and 177637 (Tomaz, 1988) with state remittances, the average yearly value of gold sent from Brazil, between 1720 and 1780, represents 79% per year of the state fiscal revenue. These comparisons, which take into consideration only the annual Brazilian gold flows, demonstrate how large the quantities received in Lisbon were.38

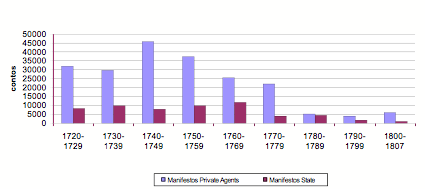

The analysis of the data per recipients and per decade allows us to form a general overview of the remittances. Of the total of gold flows between 1720 and 1807, around 77.5% was destined for the private agents and approximately 22.5% was destined for the State.39 The study of the behavior of gold remittances shows that the amounts of gold sent to private agents oscillated more than those received by the State. On the other hand, the periods of the greatest arrivals of gold do not coincide with the two largest groups of recipients. For the private agents, the high point of the arrivals was the 1740s, while the decade of the 1760s was the period of greatest net income for the State (Table 2 and Chart 4). This conclusion is highly relevant in Portuguese historiography and should be developed in future studies. Indeed, the decade of the 1760s was considered as a period of successive State crises, which justified the fiscal measures adopted by the Marquis of Pombal at the time.40 This crisis situation, explained by the fall in income from the empire, also justified a change in the direction of Pombaline policy, which after 1769 began to develop the country’s industry. The industrial policy that was adopted is deemed by Portuguese historiography to have been a response to the trade crisis which took place in the South Atlantic.41

Table 2. Average annual income (in contos)

Period |

State Annual Average |

Private Annual Average |

1720–1729 |

852 |

3202 |

1730–1739 |

1014 |

3002 |

1740–1749 |

823 |

4600 |

1750–1759 |

984 |

3754 |

1760–1769 |

1189 |

2580 |

1770–1779 |

430 |

2214 |

1780–1789 |

482 |

556 |

1790–1799 |

184 |

446 |

1800–1807 |

137 |

632 |

Sources: Manifestos, Livros dos Manifestos, Manifestos Avulsos, ACML and Livros das Frotas do Grão Pará, AHU.

Chart 5. Remittances and recipients

It is stressed that these remittances sent to the state represent net income, because the income which arrived in Portugal had already had the military and administrative costs involved in the colonial apparatus deducted from it. Therefore, there is not a direct or immediate relationship between the state income and the levies on gold (the tax known as the quinto or fifth). The flows registered in this series cannot, therefore, be taken as arising from a greater or lesser fiscal efficiency. In fact, the study of the fiscal policy relating to gold continues to be a field of important future research, since it remains to be calculated which of the taxes on gold were more efficacious in fiscal terms, whether the quinto or the capitação, this last tax having been introduced between 1735 and 1750.

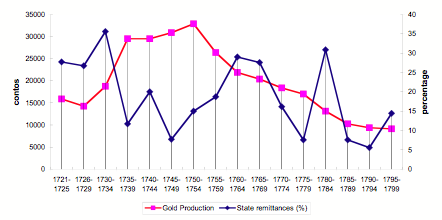

Despite the fact that net income was not confined to the quantity of tax levied on gold, the significance of this income compared with production must be understood. There are different calculations made for the quantities produced.42 However, the values presented by Noya Pinto not only represent a middle point between different estimates, but are also the least contested.

Chart 6. Gold production and State remittances (1721–1799)

Sources: For production, Virgílio Noya Pinto, op. cit., 1979, and, for State remittances, according to Livros dos Manifestos, Manifestos Avulsos, ACML and Livros das Frotas do Grão Pará, AHU.

Note: The calculations to determine the value represented by gold production were carried out by converting kilos into marks and assessing these at the legal price of gold at 96,000 réis/mark (Law of August 4, 1688).

If the comparison is based strictly on Noya Pinto’s studies on gold production in the three main mining regions, Minas Gerais, Goiás and Mato Grosso,43for the period 1721 to 1799, it can be concluded that the net income received in Lisbon was 60,954 contos (146,056 kg). Thus, the irregular movements of State income do not mirror the fluctuations of gold production. This means that the production of gold cannot be used as the only variable to explain the state remittances which arrived in Lisbon.

As far as the flows recorded for the private economic agents are concerned, if their relationship with mining production is less immediate, future studies will have to consider deeply the variables which explain the behavior of these private remittances.

In conclusion, the historiography on the precious metal trade has sought to calculate, question and discuss the more accurate values.44 In the case of Spanish silver in the 17th century, several indicators have been used to demonstrate the impossibility of the decrease in silver remittances that is traditionally highlighted and called into question by data calculated from the gazettes (Morineau, 1985). As for Portuguese gold in the 18th century, the official source, the Livros dos Manifestos, raises other historiographical issues.

Conclusions

The Livros dos Manifestos, the official Portuguese register of Brazilian gold remittances, reveals a continuity which is explained by the administrative procedures implemented by the state during the 18th century.

The payment of a 1% tax on the value of gold was justified as a protection cost until 1765, when the system of navigation in fleets was in force. When this navigation system finished, the payment of the 1% charge acquired the characteristics of both a protection cost and a tax. In the latter case, the connivance sought with the carriers of gold becomes a guarantee for the state, supporting the continuity of its fiscal position. Thus, contrary to what happened in Spain in the 17th century, the Portuguese State did not surrender its centralized fiscal position in the precious metal trade.

The tax remittances sent from the empire on the other side of the Atlantic were destined for the Lisbon Mint House, where the Royal Officials controlled the arrivals of gold. In the time span between 1720 and 1807, the Treasury obtained 22% of the total gold arrivals. This was net income, from which it is not possible to draw conclusions about the fiscal efficiency of the state. But the receipts obtained from Brazil were significant in terms of the total tax revenue. There could have been fraud and contraband, but the Portuguese State sought to control the official quantities of Brazilian gold.

The study of the Livros dos Manifestos allows us to conclude that the Lisbon Mint House centralized gold arrivals and the payment of the 1% levy on gold during the 18th century. The Iberian states followed different fiscal, monetary and administrative paths, which explains the differing credibility of official sources.

Abbreviations used

IAN/TT – Instituto dos Arquivos Nacionais / Torre do Tombo

National Archives Institute/Torre do Tombo

ACML – Arquivo da Casa da Moeda de Lisboa

Lisbon Mint House Archive

BNP – Biblioteca Nacional de Portugal

Portuguese National Library

References

Alden, Dauril (2004), “O Período Final do Brasil Colónia, 1750-1808,” América Latina Colonial, Leslie Bethel (org.), São Paulo.

Anes, Rafael Donoso (1996), Una Contribución a la Historia de la Contabilidad: Análisis de las prácticas contables desarrolladas por la tesorería de la Casa de la Contratación de las Indias de Sevilla (1503-1717), Universidad de Sevilla, 1996.

Barrett, Ward (1990), “World bullion flows, 1450-1800,” in The Rise of Merchant Empires: long distance trade in the early modern world, 1350-1750, James D. Tracy (ed.), Cambridge.

Bernal, Antonio Miguel (1987), “Libre comercio (1778): Un primer ensayo de modelo general,” El Comercio Libre entre España y America Latina, 1765-1824, Antonio Miguel Bernal (coord.), Madrid.

Bethel, Leslie (org.) (2004), História da América Latina: América Latina Colonial, vol. II, São Paulo.

Boxer, Charles Ralph (1962), The Golden Age of Brazil, 1695-1750, University of California Press, Berkeley and Los Angeles.

Boxer, Charles Ralph (1969), O Império Colonial Português (1415-1825), Lisbon.

Boxer, Charles Ralph (1979) “Descriptive list of the state papers Portugal 1661-1780” in the Public Record Office London, Lisbon: Academia das Ciências de Lisboa, 3 vol. (1661-1780).

Boyer-Xambeu, Marie-Thérèse; Deleplace, Ghislain; Gillard, Lucien (1994), “Régimes monétaires, points d’or et “serpent bimétallique” de 1770 à 1870,” Revue Économique, No. 5, Septembre, pp 1139-1174.

Carrara, Ângelo (2007), “Administração Fazendária e Conjunturas Financeiras da Capitania de Minas Gerais, 1700-1808,” Working Paper 01-07, Universidade Federal de Juiz de Fora.

Carreira, António (1983), As Companhias Pombalinas, Lisbon.

Costa, Leonor Freire; Rocha, Maria Manuela; Sousa, Rita Martins de (2005), “O ouro cruza o Atlântico,” Revista do Arquivo Público Mineiro, No. 1.

Costa, Leonor Freire; Rocha, Maria Manuela (2007), “Remessas do ouro brasileiro: organização mercantil e problemas de agência em meados do século XVIII,” Análise Social, vol XLII (182), pp. 77–98.

Cortesão, Jaime (1956), Alexandre de Gusmão e o Tratado de Madrid (1750), Rio de Janeiro.

Drelichman, Maurício (2005a), “American Silver and the Decline of Spain,” The Journal of Economic History, Cambridge University Press, vol. 65(02), pp. 532–35.

Drelichman, Maurício (2005b), “The curse of Moctezuma: American silver and the Dutch disease,” Explorations in Economic History, vol. 42(3), pp. 349–80.

Engerman, Stanley L. (1994), “Mercantilism and overseas trade, 1700–1800,” Roderick Floud and Donald McCloskey (eds.), The Economic History of Britain since 1700, vol. I, 2nd edition, Cambridge.

Fisher, H.E.S. (1984), De Methuen a Pombal – O Comércio Anglo-Português de 1700 a 1770, 2nd edition, Lisbon.

Flynn, Dennis (1996), World Silver and Monetary History in the 16th and 17th Centuries, Collected Studies Series, Aldershot, Variorum.

Frutuoso, Eduardo; Guinote, Paulo; Lopes, António (2001), O movimento do porto de Lisboa e o comércio luso-brasileiro (1769–1836), Lisbon.

Godinho, Vitorino Magalhães (1955), Prix et Monnaies, Paris.

Godinho, Vitorino Magalhães (1990), “As frotas do açúcar e as frotas do ouro, 1670–1770,” Mito e Mercadoria. Utopia e Prática de Navegar (Séculos XIII–XVIII), Lisbon.

Hamilton, Earl J. (1934), American Treasure and the Price Revolution in Spain 1501–1650, Cambridge.

Ibarra, António (2000), “El Consulado de Comercio de Guadalajara, 1795–1821. Cambio institucional, gestión corporativa y costos de transacción en la economía novohispana,” Dinero y negocios en la historia de América Latina, Nikolaus Bottcher and Bernd Hausberger (eds.).

Lopes, Paulo Alexandre Marques (2001), Minas gerais setecentistas: Uma “Sociedade Aurífera,” mimeograph, Faculdade de Letras da Universidade de Coimbra.

Macedo, Jorge Borges de (1982), Problemas de História da Indústria Portuguesa no Século XVIII, 2nd edition, Lisbon.

Macedo, Jorge Borges de (1989), A Situação Económica no Tempo de Pombal, 3rd edition, Lisbon.

Mauro, Frédéric (1991), “O Império Luso-Brasileiro, 1620–1750,” Nova História da Expansão Portuguesa, vol. VII, Lisbon.

Melgar, José María Oliva (2005), “La metrópoli sin territorio. Crisis del comercio de indias en el siglo XVII o pérdida del control del monopolio?” El sistema atlántico español (siglos XVII–XIX), Carlos Martinez Shaw, José María Oliva Melgar (eds.), Madrid.

Monteiro, Nuno Gonçalo (2006), D. José, Lisbon.

Morineau, Michel (1985), Incroyables gazettes et fabuleux métaux—les retours des trésors américains d’après les gazettes hollandaises (XVI–XVII siècles), Paris-Cambridge.

Pedreira, Jorge M. (1988), “Industrialização e flutuações económicas, preços, mercados e inovação tecnológica. Apontamentos e reflexões sobre o caso português (1670-1890),” Estudos e Ensaios em Homenagem a Vitorino Magalhães Godinho, Lisbon.

Pedreira, Jorge M. (1992), Os Homens de Negócio da Praça de Lisboa - de Pombal ao Vintismo (1755–1822), mimeograph, Lisbon.

Pijning, Ernst (2001), “Contrabando, ilegalidade e medidas políticas no Rio de Janeiro do século XVIII,” Revista Brasileira de História, São Paulo, vol. 21, pp. 397–414.

Pinto, Virgílio Noya (1979), O Ouro Brasileiro e o Comércio Anglo-Português, 2nd edition, São Paulo.

Quinn, Stephen (1996), “Gold, Silver, and the Glorious Revolution: arbitrage between bills of exchange and bullion,” Economic History Review, XLIX, 3, pp. 473–90.

Redish, Angela (1990), “The Evolution of the Gold Standard in England,” The Journal of Economic History, volume L, No. 4, pp 789–805.

Rocha, Maria Manuela; Sousa, Rita Martins de (2005), “Moeda e Crédito,” História Económica de Portugal - Século XVIII Álvaro Ferreira da Silva and Pedro Lains (org.), Lisbon.

Romano, Ruggiero (2004), Mecanismo y elementos del sistema económico colonial americano, siglos XVI–XVIII, Mexico.

Russell-Wood, A. J. (1983), “As frotas do ouro do Brasil, 1710-1750,” Estudos Económicos, 13 (special issue), pp. 701–17.

Serrão, José Vicente (1993), “O quadro económico,” José Mattoso (dir.), História de Portugal, vol. IV, Lisbon.

Sideri, Sandro (1978), Comércio e poder, colonialismo informal nas relações anglo-portuguesas, Lisbon.

Simonsen, Roberto C. (1957), História Económica do Brasil (1500–1820), 3rd edition, São Paulo.

Sindreu, Francisco de Paula Pérez (1992), La Casa de la Moneda de Sevilla Su Historia, Seville: Universidad de Sevilla.

Sousa, Rita Martins de (2006), Moeda e Metais Preciosos no Portugal Setecentista (1688–1797), Lisbon.

Sutherland, Lucy S. (1962), A London Merchant, 1695-1774, Oxford University Press.

Tomaz, Fernando (1988), “As Finanças do Estado Pombalino, 1762–76,” Estudos e Ensaios em Homenagem a Vitorino Magalhães Godinho, Lisbon.

Valério, Nuno (coord.) (2001), Portuguese Historical Statistics, INE, 2 vols, Lisbon.

Notes

* I have benefited from the valuable suggestions made by two anonymous referees. I would like to thank José Carlos Neto for his assistance in processing the data which form the quantitative database for this article. All errors in this article are entirely my own.

1 See the articles published by Mauricio Drelichman, who uses economic and institutional theory to analyze Spain’s backwardness from a historical perspective, cf., specifically, Drelichman, 2005a) and 2005b).

2 It has been calculated that from the total amount of gold issues made by the Lisbon Mint House and the Mint Houses in Brazil (especially the Mint House in Rio de Janeiro, since there are continuous data available for the 18th century), around 18% would have remained in the State’s coffers and in the hands of private agents in the period from 1688 to 1797. This percentage represents a money supply of around 55,000 contos at the end of the period. At the end of the 18th century, the degree of monetarization of the Portuguese economy was worth 17,135 réis per capita and was therefore identical to the degree of monetarization in the French economy (Sousa, 2006; Rocha and Sousa, 2005).

3 The quantitative information has been studied exhaustively, despite the great volume of information: there are around 190,000 registers dating from between 1720 and 1807.

4 The study of the source from the viewpoint of qualitative information allowed for an analysis not only of the agents involved (senders, recipients and proxies) but also an in-depth analysis of the networks of relationships existing within the trading organization between Portugal and Brazil (cf. Costa and Rocha, 2007).

5 Charter of February 1, 1720.

6 To confirm the scarcity of ledgers before the introduction of the 1% tax, it should be noted that in 1717 only 28 contos worth of gold were registered, while, in 1718 and 1719, 237 and 86 contos were registered respectively (Lopes, 2001). In 1720, the quantity of gold registered rose to 2,870 contos.

7 See Decrees of November 21, 1757, June 28, 1759, and June 30, 1759.

8 In the Charter of 1765, four reasons were given to end the fleet system, although three of these were interrelated. The degradation of the products transported was the first reason, while the other three were related to the delay in payments, explained both by the fleet system and also by the actions of some agents in Brazil. Thus, the fourth reason considered that the replacement of these agents would be speeded up if the shipping system was free.

9 In separate documentation, several requests can be found addressed to the Inspectors of the Safe for them to authorize the delivery of remittances which, despite not having been declared in Brazil, were declared in Lisbon at the time of the inspection (Manifestos da Visita do Ouro, ACML).

10 After 1765, there were two types of Manifestos: the Livros de Manifesto,which existed before the fleet system ended, were printed and came with the frigates, and the separate Manifestos, which were handwritten and fo und on separate sheets of paper or groups of sheets sewn together.

11 Discussion about the characteristics of the tax levied by the Crown on the activity of mining, the quinto or capitation tax, was based upon the efficiency of the taxation system, or rather, on the most expedite means of minimizing contraband, cf. Cortesão (1956), as well as various documents in the Lisbon National Library (BNP, Fundo Geral, Colecção Pombalina).

12 Books which cover the period between 1769 and 1773, with the reference numbers 1611 and 1612, ACML.

13 In the Registo Geral there are occasionally accounts of gold coins that were carried in the pockets of passengers in small amounts, despite the fact that larger quantities had been declared. Several examples can be found in the Registo Geral, Nos. 2 to 7, ACML.

14 Several examples can be used to illustrate these parallel circuits. One of these examples took place in 1764 when an employee of the Lagos District Council informed the King of the shipwreck of a French vessel sailing from Martinique to Marseilles laden with sugar, cocoa and coffee, as well as safes containing money, including Portuguese coins with the face value of 6$400 réis. This employee added in his information that he had arrested the sailors, because “they looked more like pirates than proper traders” (AIN/TT, Ministério do Reino, Maço 326, Caixa 437).

15 It should be stressed that not only is contraband a theme that is beyond the scope of this article, but also that nowhere in this article have we stated that the Manifestos are better than other sources because they take the illegal trade in precious metals into account.

16 The Real Cédula of March 31, 1660, states “(...) para que la plata y oro de particulares de Tierra Firme y Nueva España viniesse sin sujección a rexistro, si no es quien voluntariamente quisiere rexistrarla ... traiéndola en confiança los maestres de la plata o compradores della sin obligaçión de entrarla en la Casa de la Contratación, ni dezir ni declarar a qué dueños perteneçe (...),” quoted in Melgar, 2005: note 57, p 50 (my emphasis in bold).

The first measures appointed Cadiz as the city to build Casa de la Contratación, but in 1503 the Catholic Kings decided that Seville would be the city that centralized the Atlantic trade. The importance of the Genovese present in Seville since the 13th century to finance trade and the proximity with Castile, would have been significant reasons to support that resolution (For a brief story about Casa de la Contratación see Anes, 1996: 45–114).

17 The avería was a tax paid for the transportation of people and goods to cover expenses incurred in financing the fleets. It was administered until 1660 by the Consulado de Sevilla, except during some periods when it was rented out to private agents (Anes, 1996: 101).

18 As the fleets of Nueva España and the galleons of Tierra Firme did not travel every year, the Spanish Treasury did not actually have a fixed income, as it was supposed to receive from these fleets.

19 The Port of Lisbon hosted an enormous volume of colonial trade, representing almost 70% of the total trade at Portuguese ports in 1765. Porto was a centre for the export of wine, while Setúbal was the main centre for salt exports to northern Europe (Frutuoso, Guinote and Lopes, 2001, pp. 26–31).

20 cf. British Parliamentary Papers, “Monetary Policy: General,” volume 1.

21 According to Michel Morineau, the Dutch Gazettes made corrections because at times there were differences caused by transcription errors, and so they completed the data because the consular information omitted the arrival of some fleets (Morineau, 1980: 124–25).

22 ACML, Livros dos Manifestos, for 1742, Ledgers Nos. 2201 and 2202 and, for 1743, Ledgers Nos, 2223, 2224 and 2225.

23 These sources were, namely, the data which existed in the work by Dauril Alden, Royal government in colonial Brazil, Berkeley, Los Angeles, 1968, and the calculations made from the monetary issues from the Rio and Lisbon Mint Houses (Morineau, 1985: note 19, p. 135).

24 The separate Manifestos were studied using the criterion of the origin and/or the name of ships, carracks, galleons ... To avoid double entries, we checked all the information and considered it only when there were no references found in the previous registers or when it was possible in this way to obtain data that was illegible elsewhere, which was the case with the Manifestos da frota da Baía of 1764.

25 Remittances of gold originating from these Brazilian regions were only exempt from the 1% payment if they belonged to the companies. The Companhia do Grão Pará e Maranhão was set up in 1755. Four years later, the Marquis of Pombal set up the Companhia de Pernambuco e Paraíba. These commercial companies enjoyed a number of privileges that were brought to an end in the last two decades of the 18th century. Among these privileges was the non-payment of the 1% levy on gold from Brazil. The most detailed study of these companies continues to be that of Carreira, 1983.

26 In the Arquivo Histórico Ultramarino were Ledgers Nos. 1704, 1706, 2019 to 2038, and some separate documents in boxes Nos. 75, 77 to 79, 80, 81, 85, 86 and 102. This corresponded to 148 ledgers, an insignificant number among the millions that this research project implied.

27 1 conto = 1,000,000 réis. Réis is the plural of real, the Portuguese monetary unit between 1425 and 1911.

28 In the source, there are values with slight differences due to the quality/carats of the gold received. Not all the gold had 22 carats. However, the differences are not significant. For 1731, for example, if we use the most commonly stated value, we obtain a total of 4402 contos, whereas, using the legal value, the final amount is 4401 contos.

29 It is considered that 1 kg = 4.3478261 marks (Pinto, 1979: 335).

30 Tesoureiro da Fazenda Real was the Treasurer of the Royal Exchequer, and these receipts were correlated with several types of taxes.

31 Tesoureiro da Casa da Moeda de Lisboa was the Treasurer of the Lisbon Mint House, and some of these entries paid for the sending of materials to the Brazilian Mint Houses.

32 The Junta do Tabaco (the Tobacco Board) was one of the State monopolies.

33 Tesoureiro dos Defuntos e Ausentes was the Treasurer of Deceased and Absent Persons, and the amounts recorded were destined for the king. In Spain these Deceased and Absent Persons were afforded separate ledgers and had a separate accounting system (Anes, 1996: 63, 67, 94–100).

34 The Mesa da Consciência e Ordens (Board of Conscience and Orders) was set up in 1551 and had the power to manage financial problems until the Erário Régio (Royal Exchequer) was founded in 1761.

35 Rio de Janeiro (1702), Baía (1724) and Vila Rica (1724–1734) were the Mint Houses in Brazil. Many Portuguese coins were minted in these Mint Houses during the 18th century (Morineau, 1985; Sousa, 2006).

36 A more detailed study of the Livros dos Manifestos will be the subject of other articles.

37 The comparison between the remittances which arrived and public income is restricted to the interval between 1762 and 1776, because this is the period of the 18th century for which there is a systematic study of the public finances of the Portuguese State (cf. Tomaz, 1988).

38 In a comparative quantitative analysis, it can be confirmed that the gold flows were far more abundant in the 18th century. Considering only the gold which entered the Mint House for coining purposes, it is calculated that between 1515 and 1671, 135,570 marks (589,435 Kg) entered the country, while between 1688 and 1797, the figure was 1,026,009 marks (4,460,909 kg) (cf. Sousa, 2006: 162–65).

39 Contrary to Spain, where the values are mere estimates (Melgar, 2005), in Portugal the values are calculated from the Manifestos. The percentage calculated is close to that obtained by studies that are being undertaken by Brazilian researchers for the region of Minas Gerais, a mining region responsible for 80% of the total amount of gold extracted during the 18th century. The amount calculated from the receipts from Minas Gerais and sent to Lisbon is 620 arrobas between 1714 and 1810 (excluding the years 1722 to 1735), or, rather, 23% of the total from this region (Carrara, 2006).

40 The fiscal measures adopted were designed to increase the State’s revenue, citing the fall in income from Brazilian gold. The increase in the décima tax from 4.5% to 10% (1762) and the increase in levies on the entry of goods (1763) were some of these measures.

41 In Portuguese historiography, industrial booms have been considered as responses to trade crises (Godinho, 1955). This thesis has been subject of debate, particularly for the period at the end of the 18th century (Cf. Pedreira, 1988).

42 See Simonsen, 1957, and Pinto, 1979, where the different data are summarized.

43 Noya Pinto did not consider the production of Baía. The inclusion of this mining region in the data would increase the gold production in the period 1725–1745 (Pinto, 1979).

44 See, for instance, Barrett, 1990.

Copyright

2008, ISSN 1645-6432

e-JPH, Vol.6, number 1, Summer 2008 |

|

|