| |

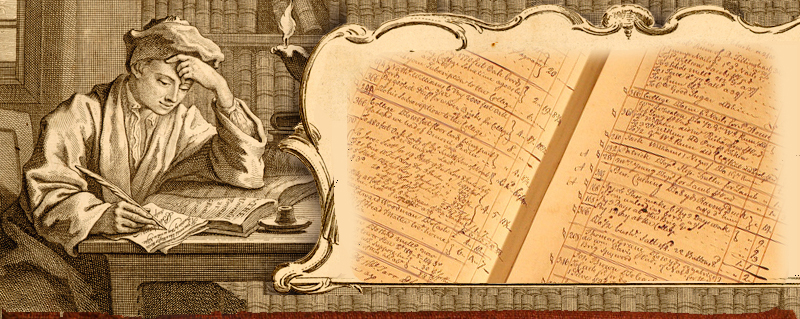

account || double entry Bookkeeping

|

BOOK-KEEPING is an art, teaching how to record and dispose the accompts of business, so as the true state of every part, and of the whole, may be easily and distinctly known.

—John Mair, Book-keeping Methodiz’d: or A methodical treatise of Merchant-Accompts, according to the Italian form. Seventh edition. Edinburgh: 1763. |

|

The clerks and businessmen represented in this exhibition were trained in the double-entry, or “Italian” method of bookkeeping. Developed by Italian merchants in the 13th century, double entry bookkeeping was the accounting standard for businesses on both sides of the Atlantic. As the name indicates, in double entry bookkeeping every financial event is entered twice in a company’s account books—as a debit and a credit—in order to track the impact of each transaction on the company’s overall balance of assets and liabilities.

For example, if a customer purchased a quantity of merchandise, the goods would be registered as a debit on the left side of the page for the customer’s account (“Dr” for debitor) and the payment given for the goods would appear as a credit on the right side (“Cr” for creditor). Ideally, debits and credits would be equal when the books were periodically “balanced.”

In the 18th century, the system relied on the use of three “books of entry”: the waste book, the day book (or journal), and the ledger. The first two books functioned as memory aids and organization tools for the entry of information into the ledger. The examples shown in this case illustrate the progress of a transaction through these books of record.

In the 1760s the Browns were involved in raising money for the establishment of the College of Rhode Island (later Brown University)—primarily by soliciting “subscriptions” from other members of the community (see Case 5). Welcome Arnold and his brother Jonathan were among these subscribers, and the books in this case trace how the Arnolds paid for part of their subscription in lime, the primary commodity in the area of Smithfield where their family lived.

|

|

| |

|

|

|

Bill for Jonathan & Welcome Arnold’s subscription to the College. February 11, 1770. Brown family business records.

This bill shows that in September 1770 both Welcome Arnold and his brother Jonathan paid for part of their subscription to the College with 10 and 12 hogsheads of lime, respectively. |

|

| |

|

|

|

Waste book, 1770–1771. Nicholas Brown & Co. Brown family business records.

A notation on September 29, 1770 shows the delivery of 4 hogsheads of lime from Welcome Arnold, delivered to the College by Samuel Arnold (not Welcome’s son, who was born in 1773). The number “619” indicates the page in which the transaction was later entered into the company’s day book. |

|

| |

|

|

|

Day book, June 8, 1768–November 7, 1770. Nicholas Brown & Co. Brown family business records.

As indicated by the waste book, page 619 contains an entry for Welcome Arnold’s lime—the numbers “8” and “366” indicate the pages on which this transaction appears in the company’s ledger |

|

| |

|

|

|

Ledger #2, 1768–1774. Nicholas Brown & Co. Brown family business records.

At a designated point in the year, transactions are entered into the final book of record, the ledger. Each account (which could be an individual—such as a customer or supplier, or a function of the business such as the “Store” or “Iron Works”) consists of a credit and debit column reflecting the values either owed by or paid to each account.

Welcome Arnold’s account on page 8 shows the delivery of the 4 hogsheads of lime, which is also recorded on page 366, showing the account of the College of Rhode Island. |

|

| |

|

|

|

List of accounting records from the counting house. Brown family business records.

This printed list shows the kinds of records that were generated and stored during the course of the Brown family’s business transactions. It was apparently used in the company’s counting house at 50 South Main Street in Providence. |

|

| |

|

|

| |

SPIKE FILES, BUNDLES, AND ACCOUNTS BOOKS

The transactions set down in the day books and ledgers were first recorded on receipts and other documents. These slips of paper (and occasionally other material, as shown in this case) were stored in a variety of methods—impaled on spikes or folded into bundles—that allowed businesses to organize and retain the evidence of their activities.

Other methods of keeping track of events and transactions are also revealed in this case. Memoranda books, personal day books, and laborers books allowed businessmen to record and analyze different kinds of activities, many of which would be incorporated into the main books of record, such as the ledger. |

|

|

Spike file records, 1773-1774. Brown family business records.

Bills of credit, receipts for goods, promissory notes, and all manner of records used in transactions were often stored on metal spikes, piled up in the order received. Some of the records transferred to the Library from the counting house arrived on their spikes, undisturbed since the 18th century.

The Brown family’s spike files include two bills of credit written on unconventional materials. Though made of wood and slate, these bills include the tell-tale hole of the spike.

|

|

|

Bill of credit, written on wood. 1773 or 1774. Brown family business records.

“Let Dredfull Carter have Two Shillings and Six Pence Martin Seamans” |

|

|

Bill of credit, written on slate. July 16, 1774. Possibly by Joseph Brown. Brown family business records.

“N. B. & Co. Let [?] have four or five shillings & charge [?] Brown. July 16 1774” |

|

| |

|

|

|

“Bills Settled from Jany 1 to Dec. 31 1780.” Arnold family business records.

From the 18th through the 19th century, records were also stored in bundles—with each document folded, docketed (identified on the back with the type of record and date), and then piled, labeled, and tied. The Library’s collections for both the Brown and Arnold families hold a number of these bundles, still bound and waiting to be uncovered. |

|

| |

|

|

|

Memorandum book, 1782 – 1784. Arnold family business records.

In addition to the primary books of record, most 18th and 19th century businesses also used other account books to track different kinds of activities. Books of “memoranda” recorded a wide variety of often more informal transactions, as with this notation by Welcome Arnold, regarding a wager made for a beaver hat. A notation in the margin indicates that the wager was settled, but it does not say in whose favor.

“Memo. I have bet a bever hat with Mr. L. [Dilyse] that the Sloop F. America Cap Williams [will?] arrive in this River on or before the Thursday of Septr. next—Sd sloop sailed the 14 July or after W Arnold” |

|

| |

|

|

|

Day books of William E. Tillinghast, 1801–1811. Tillinghast family business records.

Some merchants and other men of business kept personal day books, much in the way people do today, to track day-to-day affairs. William E. Tillinghast used these distinctive journals for both his personal and business accounts—each with a back pocket lined with decorative paper for holding loose documents. |

|

| |

|

|

|

Laborers book, 1790. Arnold family business records.

Laborers’ books were used to track transactions between a business owner and the individuals who were hired to perform all kinds of tasks for the company. These account books prove particularly useful to researchers investigating the day to day interactions of ordinary people.

Account books often reveal long-standing relationships between business owners and individuals. The account of Mintus Martin with Welcome Arnold offers an example of an enslaved man who serves repeatedly on Arnold’s vessels. The complexity of labor arrangements in the 18th century are indicated by the accompanying letter from John Lillibridge, demanding Martin’s wages on behalf of his owner, Lillibridge’s mother-in-law. On the second page of Martin’s entry, a note from Lillibridge’s wife acknowledges receipt of the payment. |

|

| |

|

|

|

John Lillibridge to Welcome Arnold, February 21, 1790. Arnold family business records.

Being Sufficiently & duly Inform’d that my mother in Law’s Negro man named Amyntus Is gon to Se in one of your Vessel & In your Employ. This Sir is to acquante you. By the Immidiate request of my Mother in Law Rebecca Martin of Jamestown & Connanicut, That no Dispute may arise hereafter as he is a runaway & duly advertis’d. She prays you to Stop his Wages in Your Hands & not to pay him one Farthing Till an Order is presented from his mistress. She further prays you immidely on his arrival to Send Word to me in Newport As I shall come up to fetch him home when I can find he is there & in thus complying Sir you oblige Your Freind & Humble Servant . . . |

|

| |

Exhibition may be seen in Reading Room from September 12 through

december 2012.

Exhibition prepared by Kim Nusco, Reference and Manuscript Librarian, John Carter Brown Library |

|